What is a Flat Fee Financial Planner?

- Stephen Boatman

- Mar 6, 2024

- 5 min read

Updated: Apr 16, 2024

A flat-fee financial planner charges a flat monthly fee for comprehensive financial planning services, as opposed to a commission-based fee structure, an AUM (Assets Under Management) fee structure, or a combination of the two. Suppose you are looking for a transparent relationship where you can always understand what you are paying for the service you are receiving. In that case, the flat-fee financial planning structure is the most consumer-friendly. And as dollar amounts grow past $600k the respective fee can often be lower with a flat fee financial planner for clients when compared to the other options.

What Type Of Fees To Expect

Most Flat-Fee Financial Planners charge a monthly fee ranging from around $400/mo to $4,000/mo. However, if you have less than $2 million to invest, your monthly fee will likely be between $400/mo and $1,000/mo, depending on the firm.

Also, within a flat-fee-fee only financial planning firm, you won't have to worry about the three fees below that AUM and commission-based advisors may charge.

12b-1 fee: A kickback fee advisors can receive from mutual funds for investing their clients' money in them.

Product Commissions: Some advisors are paid hefty commissions for selling life insurance, disability insurance, annuities, and long-term care insurance policies. Some of these commissions are light, and I don't see a huge problem with them. However, heavy commission products such as large annuities and whole life insurance products can incentivize advisors to recommend a solution that may not be best for the client and create illiquidity issues for them in the future.

Front and deferred loads: Some mutual funds charge front-load fees when the advisor purchases the fund, which can be as high as 5.25%. If the advisor regularly buys and sells your investments, they can sell and re-purchase another front-loaded asset every 4-5 years, causing a large drag on your portfolio. Deferred loads are the same one-time large fee on top of the annual fee. However, a deferred load is triggered when the holding is sold.

These are all fees that flat fee-fee-only financial planners don't charge.

Potential Flat Fee Financial Planner Benefits

The main benefit of working with flat fee financial planners is reducing the overall fee clients pay their advisors. This benefit is difficult to realize until assets reach $600,001 (if their fee is $500/mo), but the savings can quickly escalate. This is dependent on the fee the advisor charges. The other goal is also to align incentives between the client and the advisor. The goal should be to grow the clients' net worth regardless of whether it's paying down debt, investing in alternative assets, or keeping money in a savings account/opportunity fund. The flat fee advisor is paid the same regardless. This incentive alignment helps them think clearly about the entire financial picture, not just the product that can be sold or how many assets can be brought under management.

Should Your Fee Be Based On Asset Levels?

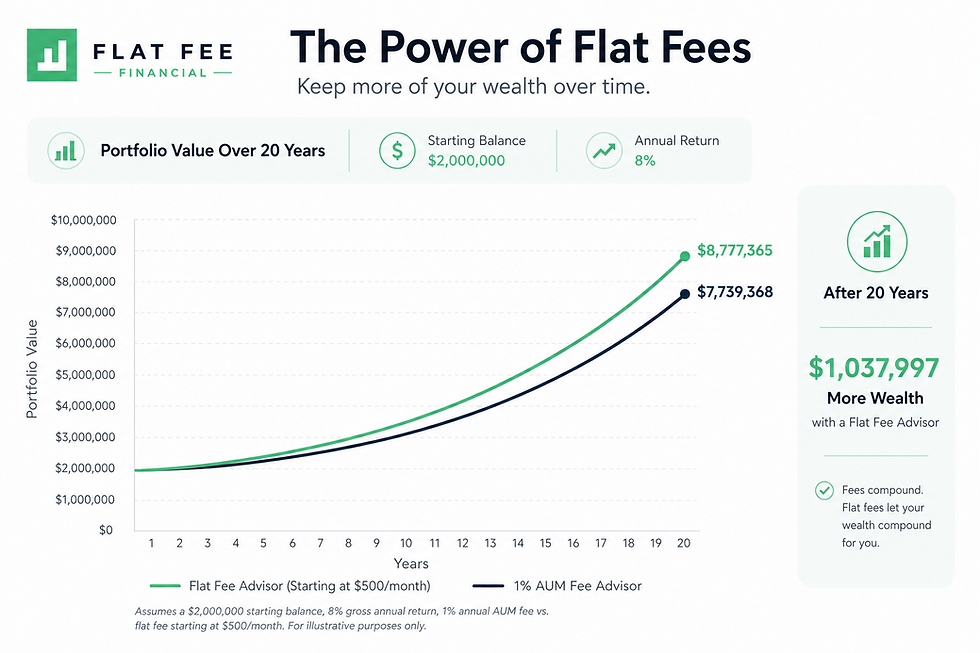

Managing a client with $1.5 million in assets isn't that much more difficult than managing a client with $1 million in assets. However, an advisor with a 1% AUM fee charges $15,000 to manage the $1.5 million portfolio and $10,000 to manage the $1 million portfolio. Alternatively, a shop like ours at Flat Fee Financial would charge a flat rate of $6,000 until assets reach $2.5 million. This impact of choosing a flat fee financial planner on the clients' possible annual withdrawal, overall net worth, and aligning incentives starts to lean heavily in the client's favor.

Focused on Client goals, not Assets Under Management Growth

Unlike advisors compensated through AUM models, flat-fee financial planners are incentivized to focus on their client's financial goals rather than the growth of their assets under management. This approach aligns the advisor's interests with the client's, creating a partnership to achieve specific milestones such as retirement planning, debt reduction, or saving for major life events. It also opens the advisor up to considering investments that aren't in the stock market.

Conflicts of Interest

Due to the fee structure of flat fee financial advisors, they may be inclined to take on less investment risk because there isn't an underlying desire to grow AUM as aggressively as their fee isn't directly tied to the firms' portfolio growth. But I would argue that you'd want someone less emotionally attached to the performance of your portfolio, as having fewer emotions involved with investment returns tends to lead to a better investor temperament and can sometimes lead to higher overall returns with a steady head at the helm.

Market Movements

AUM financial advisors have a steady increase in their fees as the market causes their clients' portfolios to increase in value. If I were the client, I would want to retain those gains for my family and other financial goals.

No Pressure To Sell Financial Products

Since flat-fee financial planners are not reliant on earning commissions from financial product sales, there's no pressure to push specific investments or insurance policies due to an underlying kickback. This freedom allows them to provide objective advice tailored to the client's best interests. Clients can rest assured that recommendations are based on their needs rather than the advisor's financial incentives or what product pays the highest commission.

Transparent and Predictable

One of the primary advantages of opting for a flat-fee financial planner is the transparency it brings to the table. With a fixed fee, clients know exactly what they are paying for financial services. This clarity contrasts sharply with the traditional model, where advisors may earn commissions on products sold or a percentage of assets under management (AUM). Flat fees eliminate the potential for hidden costs or conflicts of interest, fostering a relationship built on trust.

How Much Do Flat Fee Financial Advisors Charge?

I can't speak to all flat fee financial planning shops, but our fees are represented in the image below. $500/mo until assets reach $2.5 million, where the fee is raised to $1,000/mo until assets reach $5 million, where the monthly fee is capped at $2,000/mo. Flat fee financial planners can easily be in the .5% (annual fee) or less range as assets grow which is around 50% less expensive than the 1% aum financial planning shops.

Conclusion

In the quest for the best financial planner for your specific scenario, choosing a flat-fee financial planner can be a game-changer. With transparent pricing, a focus on client goals, and a holistic approach to financial planning, flat fee financial planners are reshaping the way individuals access and benefit from financial advice. As the financial landscape continues to evolve, the appeal of flat fee financial planners is likely to grow, offering a path to financial empowerment and well-informed decision-making for all.